Financial Tips for College Students: 9 Ways to Save & Thrive

College is where you’re supposed to be learning, but nobody hands you a manual on how to avoid financial disaster while you’re at it.

A national survey found that 59% of college students have considered dropping out due to financial stress, and nearly 80% say money problems actively mess with their mental health.

While this is more of a systematic failure, you can still avoid most of this financial disaster on your own.

This guide explains how.

Read it and learn 9 financial tips for college students to nerd out on money and actually keep some of it.

Let’s get straight into it.

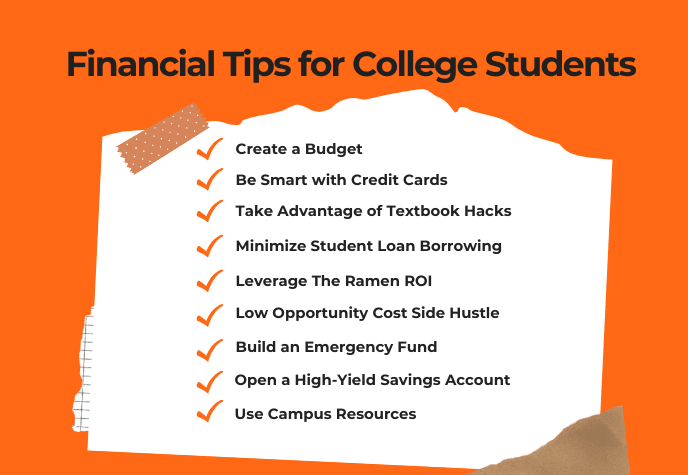

9 Best Financial Tips for College Students

Between tuition, late-night pizza runs, and that overpriced textbook you’ll sell back for $3, money vanishes faster than your expectations.

But fear not, because this list of financial advice for college students will help you dodge the worst money mistakes and maybe even graduate without a small mountain of debt.

1. Create a Budget

“A budget (for your money) is telling your money where to go instead of wondering where it went.” - John Maxwell.

The problem is that most students treat their bank balance like a mystery box. They check it only when things get dire.

Trust me, you wouldn’t want to end up like those students. And budgeting saves you from it.

Without a budget, you are simply guessing how much you can spend, and chances are, you're guessing wrong.

You can start by tracking your income sources, like parental support, part-time jobs, scholarships, etc.

Then, line up your fixed expenses: rent, utilities, transportation, and yes, that Netflix subscription you definitely need for "stress relief."

Next, you layer on your variable expenses like food, supplies, and entertainment. Factor in some for emergencies because life will, without fail, throw an economic banana peel your way.

If you’re app-savvy, try apps like Mint and YNAB (You Need A Budget). But if you’re more analog than app-savvy, a budget can be created on Google Sheets, too.

Whichever way you choose, CREATE A BUDGET! And don’t forget to update it on a regular basis.

2. Be Smart with Credit Cards

The allure of credit cards is strong, especially when you're offered a free pizza or a branded water bottle just for signing up.

Companies love handing them to students because, statistically, you’ll overspend and pay insane interest.

But what they don’t tell you is that the interest will devour you like a pack of underfed SAT tutors.

Many students fall into the minimum payment trap, not realizing that a $1,000 balance at 18% APR takes 7+ years to pay off if you only chip away at it.

The danger lies not in using a credit card but in misusing it. So, if you must get one, treat it like a debit card, keep receipts, and don’t trust it unsupervised.

Use your card strictly for planned purchases you can pay off in full every month. If you can’t, you’re spending money you don’t have.

Additionally, monitor your credit score via apps, and stay alert for unnecessary fees or missed payments.

If you're looking to build credit safely, a secured credit builder card like Firstcard can be a smart first step without the risk of falling into deep debt.

And remember the saying from Jay-Z: “If you can’t buy it twice, you can’t afford it.”

In other words, if you’re about to swipe your card for $150 shoes you can’t buy again without crying, put them down and moonwalk away.

3. Take Advantage of Textbook Hacks

$300 for a book you’ll read twice, maybe, is criminal.

Fortunately, there are workarounds.

First, check with professors if an older edition is acceptable. Most of the time, the only difference is the page numbers and a new cover photo of someone looking academically distressed.

You can also look up sites like ThriftBooks, Chegg, and eBay for cheap, used copies. Even better, check your campus library. Many keep textbooks on reserve. You’ll have to read it there, but hey, free is free.

Some students form "book co-ops" where they share textbooks within their group.

If the professor says, "You’ll need the latest edition all semester" (which is 95% identical to the last one), wait until Week 1 to confirm. Half the time, it collects dust.

You can also explore digital rentals through platforms like VitalSource or Amazon, which often cost less and don’t require you to lug around a textbook the size of a golden retriever.

4. Minimize Student Loan Borrowing

The average student loan debt balance in 2024 was $38,005.

You mustn’t let your debt snowball like this.

Make it a habit to only borrow what you absolutely need. Just because you can borrow more doesn’t mean you should.

When loans become necessary, stick to federal loans over private ones. Federal loans usually have lower interest rates, income-driven repayment plans, and deferment options if life goes haywire post-graduation.

If you already have loans, take time to understand how interest accrues and whether you can make interest-only payments while in school to prevent ballooning debt.

And please, please—know the difference between subsidized and unsubsidized loans. The former lets you breathe during college without accruing interest, while the latter starts the debt meter from day one.

Federal vs Private Loans Comparison Table:

5. The Ramen ROI

“Live like a student now, so you don’t have to later.”

Yes, you can live frugally without living miserably. Financial literacy for college students also involves eating well without torching your budget.

Start with food. Ramen is a cliché for a reason: it’s dirt cheap. But malnutrition isn’t a flex, either.

Evaluate your meal plan costs versus actual usage. If you're only on campus three days a week, why are you paying for 21 meals? So, adjust accordingly or opt for smaller plans.

Cooking at home is the MVP of cost-saving. And no, it doesn’t have to be sad. Simple meals—stir fry, pasta, eggs ten ways—are cheaper than a $14 Chipotle bowl that vanishes in six minutes.

Take full advantage of YouTube for this purpose and learn at least five cheap yet healthy meals.

Table for a Weekly Budget Meal Plan for One:

6. Side Hustle with Low Opportunity Cost

Find side hustles that don’t drain you academically or socially.

Even better if it ideally aligns with your schedule and skills. For example, tutoring fellow students not only pays, but also reinforces your knowledge.

If you aren’t good at tutoring but can code, write, or even organize closets, someone out there will pay you.

Freelance gigs are also flexible and can be done from the comforting confines of your dorm.

Dig up platforms like Fiverr, Upwork, and campus job boards, and you’ll find a hustle of your interest.

To make a few extra bucks from home, you can also turn to get-paid-to-play platforms like Scrambly and play games or use apps that pay real money and gift cards.

Check out Scrambly7. Build an Emergency Fund

Unexpected expenses will happen (broken laptop, flat tire, medical copay), so don’t sleep on building an emergency fund. This is one of the most important financial tips for college students.

And no, you don’t have to build it overnight. Even $10 a week socked away can compound into a safety net over a semester. Aim for $500 to start, then build towards $1,000.

To make this automatic, set up a recurring transfer from your checking to savings every payday.

This fund must remain sacred. Not for concert tickets. Not for pizza. Only visit it when life delivers a punch, and your regular budget can’t absorb the hit.

8. Open a High-Yield Savings Account

If you’re keeping your savings in a traditional account with a 0.01% interest rate, congratulations—you’re losing to inflation.

Instead, open a high-yield savings account.

These accounts, offered by online banks like Ally, Discover, or Capital One, typically offer 4%+ APY as of recent months.

These accounts are FDIC-insured, safe, and designed for long-term savers. It’s important to choose one with no monthly fees and no minimum balance requirement. You can link it to your checking account and automate transfers.

9. Use Campus Resources

One of the most painfully overlooked things in money management for college students is using the resources already baked into your tuition.

Most students don’t use them. Because they forget, or worse, they don’t know these exist.

To be in the know about them, make it your mission to attend orientations, read the bulletin boards, and befriend the people behind the student services desk.

FAQs on Money Management For College Students

What is the best way to budget as a college student?

The best way is to track all your income and expenses using a simple budgeting app or spreadsheet. Stick to the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings or debt. Review your budget weekly to stay on track.

What are the top 3 financial habits?

The top 3 financial habits could be the following:

- Spend less than you earn

- Save consistently (even small amounts)

- Avoid high-interest debt like credit cards

These habits help you stay financially stable in the long run.

How much should I save each month?

As a student, aim to save at least 20% of your monthly income, if possible. If that’s too much, start with what you can. Consistency matters more than the amount here.

Scrambly: Play Games and Earn Real Money as a Student

With that, you’ve got a practical blueprint of financial tips for college students that actually work.

Budgeting, side hustles, and smart use of resources are survival skills in the modern college economy.

It’s even better if you find a way that turns your recreation time into a side income, even if it is a lazy one.

And Scrambly is a ready-to-use solution like that, exactly. With it, you can earn extra money by simply playing games or trying apps.

You’ve got over 200 games and apps to try, super low payout thresholds (as low as $1), and instant withdrawals to PayPal or as gift cards.

Download Scrambly Now